Non classé

Why Undersea Internet Cables Matter to Global Supply Chains

Published

2 mois agoon

By

Global supply chains do not run only on ships, ports, warehouses, and trucks. They also run on data. Undersea cables are becoming part of the same infrastructure risk conversation as canals, straits, pipelines, power grids, cloud platforms, and payment networks.

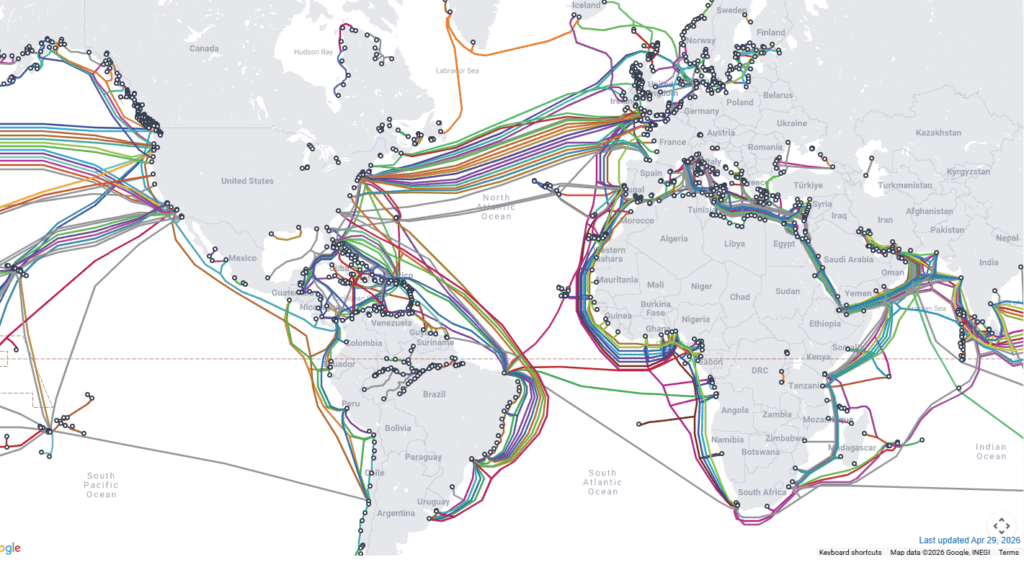

Undersea Cables Are Supply Chain Infrastructure

For most of modern logistics history, the word “chokepoint” meant a physical place.

The Strait of Hormuz. The Suez Canal. The Panama Canal. The Strait of Malacca. A congested port. A rail corridor. A border crossing. A bridge.

That definition is now too narrow.

Global trade also depends on digital chokepoints. These are less visible than ports and canals, but they are increasingly central to the movement of goods, money, documents, instructions, and commitments. Beneath the ocean floor, submarine fiber-optic cables carry the data layer of the global economy. They support financial transactions, cloud computing, customs documentation, logistics visibility, port systems, carrier communications, manufacturing coordination, and the routine exchange of commercial information that allows supply chains to function.

The recent discussion by Iranian-linked media about fees, permits, and potential control over undersea internet cables passing through the Strait of Hormuz is a useful reminder of this shift. The Strait of Hormuz has long been understood as an energy and maritime chokepoint. The newer concern is that the same geography may also become a digital pressure point.

That does not mean a disruption is imminent. It does mean supply chain leaders need to broaden how they think about infrastructure.

The supply chain is no longer only physical. It is physical, financial, digital, and computational at the same time.

The Digital Layer of Trade

Modern supply chains require continuous information flows.

A container move depends on booking data, customs filings, bills of lading, port community systems, carrier status updates, bank payments, purchase orders, warehouse instructions, customer notifications, and inventory commitments. A disruption in physical movement is obvious. A disruption in digital movement can be less visible at first but can rapidly affect execution.

If transportation management systems cannot receive status updates, visibility degrades. If customs platforms slow down, cargo can be delayed. If payment networks are disrupted, commercial settlement becomes uncertain. If cloud services or data routes become unstable, companies may lose access to systems that manage planning, fulfillment, sourcing, and customer communication.

This is why undersea cables should be understood as supply chain infrastructure.

They are not peripheral telecommunications assets. They are part of the operating environment for global logistics.

Hormuz as a Digital Chokepoint

The Strait of Hormuz is already central to global energy flows. Its role in oil and gas markets is well understood. What is receiving more attention now is the overlap between energy routes, maritime routes, and data routes.

The operating significance is not whether a particular proposal becomes formal policy. The significance is that undersea cables are being discussed in the same strategic vocabulary historically applied to oil tankers, naval transit, and regional trade.

That is the change.

Digital infrastructure is now part of geopolitical bargaining.

A country does not need to stop container vessels to create supply chain pressure. It can threaten energy flows, interfere with port systems, disrupt payment channels, target cloud infrastructure, or place legal and operational pressure on communications networks. The practical effect can be similar: greater uncertainty, higher risk premiums, slower execution, and reduced confidence in the reliability of trade lanes.

This matters because supply chains increasingly depend on near-real-time information. Visibility platforms, transportation management systems, supplier portals, customs systems, warehouse systems, and customer service applications all assume that the data layer will remain available.

That assumption deserves more scrutiny.

Why This Matters to Supply Chain Executives

Most supply chain risk programs are still built around familiar categories: supplier failure, port congestion, natural disasters, labor disruption, geopolitical conflict, cyberattack, inventory shortages, and transportation capacity.

Those categories remain valid. But they do not fully capture the infrastructure dependencies now embedded in supply chain operations.

The modern supply chain depends on several connected infrastructure layers:

Physical infrastructure: ports, roads, rail, warehouses, airports, canals, ships, and trucks

Energy infrastructure: fuel, electricity, LNG, refining, and grid stability

Digital communications infrastructure: undersea cables, terrestrial fiber, satellite backup, and telecom networks

Computational infrastructure: cloud platforms, data centers, AI systems, and enterprise applications

Financial infrastructure: payments, trade finance, insurance, credit, and settlement systems

A shock in one layer can cascade into others.

A maritime conflict may raise fuel prices and delay cargo. It may also affect cable security, cloud access, payment confidence, insurance pricing, and carrier risk calculations. A cyberattack may begin in software but interrupt physical operations. A data center disruption may affect inventory planning, customer service, and freight execution.

Supply chain resilience therefore cannot be limited to inventory buffers and alternate suppliers. It must include digital continuity.

Visibility Platforms Depend on Invisible Infrastructure

There is irony in the current technology environment. Supply chain visibility platforms are sold on the promise of knowing where everything is. But the platforms themselves depend on infrastructure that is mostly invisible to users.

Container tracking, predictive ETAs, supplier portals, warehouse dashboards, and transportation control towers all depend on the movement of data. That data often crosses national boundaries, cloud regions, telecom networks, and undersea routes before appearing as a dot on a screen.

When those communications pathways are stable, they disappear into the background. When they are threatened, the enterprise discovers that visibility is not simply a software capability. It is an infrastructure dependency.

This becomes more important as supply chains become more AI-enabled. AI systems need real-time signals, external context, transaction histories, exception data, and access to enterprise systems. The more supply chain decision-making depends on continuous data access, the more exposed it becomes to communications infrastructure risk.

AI does not reduce infrastructure dependency. In many cases, it increases it.

A supply chain that uses AI for demand sensing, dynamic routing, supplier risk monitoring, customs documentation, and customer service automation may be more responsive than a traditional supply chain. But it may also become more dependent on data availability, system interoperability, cloud access, and secure communications.

That does not argue against AI. It argues for a more complete resilience model.

The New Infrastructure Questions

For years, companies asked whether their suppliers were dual-sourced, whether their ports had alternatives, whether their carriers had capacity, and whether their inventory policies were resilient.

Those questions still matter.

But new questions are emerging:

What digital infrastructure supports our most critical supply chain workflows?

Which cloud, telecom, cable, and data exchange dependencies are embedded in our operations?

Do key logistics, planning, and visibility systems have regional redundancy?

Which workflows fail if real-time data is degraded?

Can we operate in a limited-connectivity mode?

Are escalation procedures defined for digital infrastructure disruption?

Do supplier portals, customer portals, and carrier integrations remain usable under degraded conditions?

These are not traditional supply chain questions. But they are becoming operationally relevant.

The executive issue is not whether a supply chain manager should become a telecom engineer. The issue is whether the organization understands the dependencies that support its ability to plan, execute, communicate, and recover.

Digital Chokepoints Behave Differently

Digital chokepoints are not identical to physical chokepoints.

A blocked canal is visible. A damaged bridge has a location. A closed port has a queue. A data route may degrade in more complex ways. Traffic may reroute. Latency may increase. Systems may remain partially available. Some applications may function while others fail. The business impact may depend on architecture, redundancy, vendor configuration, cloud region, access rights, cybersecurity posture, and contractual service levels.

This makes digital infrastructure risk harder to see and harder to assign.

It can sit between IT, supply chain, risk management, procurement, legal, and finance. Everyone may own part of it. No one may own the full operating consequence.

That is the governance gap.

A modern supply chain resilience program should identify which digital services are mission-critical, who owns their continuity, how disruptions are escalated, and which manual or alternate processes can sustain operations when systems degrade.

Resilience Under Degradation

The answer is not to build a fully redundant version of every system. That is unrealistic.

The better approach is to tier workflows by operational criticality.

Some workflows can tolerate delay. Some cannot. A weekly analytics report can wait. A customs filing, shipment release, carrier tender, customer commitment, or production signal may not.

Supply chain leaders should work with IT and enterprise risk teams to classify critical workflows, map system dependencies, and define continuity requirements. This includes not only core enterprise applications, but also third-party logistics platforms, visibility providers, supplier portals, carrier networks, payment systems, and external data sources.

The practical goal is resilience under degradation, not perfect immunity.

Can the enterprise still prioritize shipments? Can it still communicate with carriers? Can it still release orders? Can it still issue customer updates? Can it still make inventory allocation decisions? Can it still comply with regulatory requirements?

If not, the organization has a digital infrastructure exposure.

Conclusion: The Supply Chain Runs on Data

The supply chain has always depended on infrastructure. What has changed is the definition of infrastructure.

Ports and ships still matter. So do roads, railroads, warehouses, canals, and aircraft. But the supply chain also runs on fiber-optic cables, cloud platforms, data centers, payment networks, cybersecurity systems, and enterprise software.

Undersea cables are a reminder that the digital economy is not weightless. It has physical routes, landing points, repair constraints, ownership structures, jurisdictional exposure, and geopolitical risk.

For supply chain leaders, the lesson is clear.

Digital infrastructure is now supply chain infrastructure.

The companies that understand this will build more complete resilience programs. The companies that do not may discover, during the next disruption, that their physical network can still move goods, but their digital network cannot support the decisions required to move them wel

The post Why Undersea Internet Cables Matter to Global Supply Chains appeared first on Logistics Viewpoints.

You may like

Non classé

How Supply Chain Technology Providers Can Build Market Visibility with Research, Webinars, Podcasts, and Thought Leadership

Published

1 jour agoon

26 juin 2026By

Supply chain technology markets are crowded, complex, and changing quickly. Buyers are trying to separate durable capabilities from short-term claims, while solution providers are trying to explain where they fit in a market shaped by automation, AI, labor constraints, global disruption, network complexity, and rising expectations for operational performance.

In that environment, visibility alone is not enough. Providers need credibility, context, and market education. They need ways to reach the right audience with substance, not just promotion.

For many supply chain, logistics, transportation, warehouse automation, planning, visibility, global trade, and decision-intelligence providers, the challenge is not simply getting in front of the market. The challenge is helping the market understand why a capability matters, how it fits into broader operating realities, and what buyers should consider as they evaluate options.

That is where Logistics Viewpoints and ARC Advisory Group can help. Through market research, advisory services, sponsored thought leadership, webinars, podcasts, supplier spotlights, and industry event sponsorships, companies can engage the supply chain market in a more substantive way.

This article introduces a series on how supply chain technology providers can build credibility, visibility, and executive engagement through research, advisory services, sponsored thought leadership, webinars, podcasts, supplier spotlights, and industry sponsorships.

Over the next several posts, this series will look at each path in more detail, including when it is most appropriate, how it supports market education, and how companies can use it to strengthen positioning, credibility, and demand generation.

Market Visibility Has Changed

There was a time when visibility could be built largely through advertising, trade shows, press releases, and sales outreach. Those tools still have a role, but they are no longer sufficient by themselves.

Supply chain executives are operating in a more complex environment. They are evaluating technology in the context of labor availability, network volatility, service expectations, inventory policy, automation strategy, AI adoption, sustainability goals, regulatory change, and global risk. A narrow product message can easily get lost if it is not connected to the larger market conversation.

That is why market education matters. Buyers need help understanding what is changing, why it matters, and how different approaches should be evaluated. Providers that can contribute to that education are better positioned to build trust.

Research Helps Clarify the Market

Research is often the starting point for stronger positioning. A custom market research study can help a company answer specific strategic questions, test assumptions, evaluate market demand, understand buyer priorities, or explore a new category.

Standard market research can provide a broader foundation. It can help companies understand market size, technology adoption, competitive structure, and investment trends. For companies operating in complex supply chain technology categories, research can support product planning, executive alignment, sales enablement, and market messaging.

Annual advisory support adds another layer. It gives companies recurring access to analyst perspective throughout the year, helping them interpret market signals, refine positioning, and stay aligned with industry direction.

Thought Leadership Builds Credibility

Market credibility is not built through claims alone. It is built through perspective. Companies need to show that they understand the problems their buyers face, the tradeoffs involved, and the direction of the market.

Logistics Viewpoints sponsorship, webinars, podcasts, and supplier spotlights can all support this goal in different ways. Sponsorship provides sustained visibility in front of an engaged supply chain audience. Webinars allow companies to explain complex issues in depth. Podcasts create room for executive perspective and market narrative. Supplier Spotlights help clarify company positioning through an analyst-framed discussion of strategy, capabilities, and differentiation.

The strongest thought leadership does not begin with a product pitch. It begins with a market problem. It helps the audience understand the issue, evaluate possible responses, and connect the discussion to broader operational priorities.

Events Create Strategic Market Presence

Some conversations are best developed through direct industry engagement. Events bring together executives, practitioners, analysts, technology providers, and decision-makers around the issues shaping the future of operations.

ARC Industry Forum sponsorship gives companies an opportunity to connect their brand and message with a broader executive audience. For organizations focused on supply chain, logistics, manufacturing, automation, industrial technology, infrastructure, and enterprise transformation, this can be a way to participate in the strategic conversations that influence market direction.

Choosing the Right Path

The right program depends on the business objective. A company looking to answer a specific strategic question may begin with custom research. A team that needs recurring market perspective may benefit from annual advisory support. A provider seeking broader awareness may look at Logistics Viewpoints sponsorship. A company with an educational story may choose a webinar. An executive team with a strong market point of view may choose a podcast. A supplier that needs clearer positioning may pursue a Supplier Spotlight. A company looking for strategic industry presence may consider ARC Industry Forum sponsorship.

These programs are not mutually exclusive. In many cases, the strongest market engagement strategy combines research, advisory insight, thought leadership, and audience activation. Research can clarify the market. Advisory can sharpen the strategy. Webinars and podcasts can educate the audience. Sponsorship can sustain visibility. Supplier Spotlights can reinforce positioning. Industry events can deepen executive engagement.

The common thread is credibility. In a noisy market, buyers respond to clarity, relevance, and substance. Companies that can explain where the market is going, why it matters, and how they help customers respond will be better positioned to earn attention and trust.

For supply chain technology and logistics providers, the opportunity is not just to be seen. It is to be understood.

Explore the Series Resources

For companies evaluating the best way to build market visibility, the following program overviews provide more detail:

Custom Market Research Study

Annual Contract Advisory Service

Standard Market Research Report

Logistics Viewpoints Sponsorship Program

Sponsored Webinar Program

Sponsored Podcast Program

Supplier Spotlight Program

ARC Industry Forum Sponsorship

If you have questions about which type of program fits your company’s market objectives, reach out to me directly at jfrazer@arcweb.com. I’d be glad to discuss where your priorities align with the Logistics Viewpoints and ARC Advisory Group editorial, research, and market engagement calendar.

The post How Supply Chain Technology Providers Can Build Market Visibility with Research, Webinars, Podcasts, and Thought Leadership appeared first on Logistics Viewpoints.

Non classé

Supply Chain and Logistics News Weekly Round Up June 22nd-26th 2026

Published

1 jour agoon

26 juin 2026By

The global supply chain landscape is currently defined by rapid transformation and persistent volatility. This week’s developments underscore a shift toward greater operational resilience and adaptation, ranging from the immediate impact of the CBP’s suspension of the de minimis exemption to the mounting pressure of early peak season rate spikes. As shippers navigate these headwinds, we are also seeing structural long-term pivots, including significant federal investments in domestic nuclear manufacturing and a fundamental rethink of Transportation Management Systems—moving away from traditional software toward integrated, outcome-driven operating models. This week’s round-up explores how these forces are reshaping procurement, execution, and strategy for logistics professionals.

The End of De Minimis: CBP Suspends Low-Value Duty-Free Imports

In a monumental shift for cross-border e-commerce, U.S. Customs and Border Protection (CBP) has implemented an interim final rule that indefinitely suspends the de minimis administrative exemption, which previously allowed shipments valued at $800 or less to enter the country duty-free with minimal clearance. As detailed in the Federal Register Interim Final Rule, all commercial imports arriving via ocean, air, and trucking lanes must now undergo formal or informal customs entry procedures, exposing them to standard tariffs and rigorous compliance checks. The sudden change, also highlighted in the official U.S. Customs and Border Protection Press Release, temporarily spares only the international postal network under a strict, flat-rate tariff structure. For direct-to-consumer (DTC) brands that have built entire supply chains around direct-from-factory shipping, this regulation effectively erases their primary cost advantage overnight. Logistics planners must now scramble to transition from fragmented individual parcel shipping to bulk ocean freight, bonded warehousing, and localized domestic distribution strategies to absorb the sudden surge in operational costs and clearance times.

Ocean Freight Spot Rates Surge as Early Peak Season Collides with Port Congestion

Global container freight markets are experiencing severe pricing pressure as an exceptionally early peak season collides with systemic network constraints. According to the latest Locada Intelligence Report, spot rates from Asia to the U.S. West Coast have jumped by over 23% to cross $6,800 per FEU, while East Coast routes have surged past the $8,100 threshold. This dramatic spike is being driven by sustained shipping diversions away from the Red Sea, acute port congestion, and a preemptive rush by retailers to front-load holiday inventory. With major carriers signaling further general rate increases that could push spot rates toward $10,000 per FEU on key lanes, shippers are urged to diversify their transport modes, secure capacity early, and prepare for a highly volatile and expensive third quarter.

Shoring Up the Grid: DOE Injects $17.5 Billion to Rebuild the Domestic Nuclear Supply Chain

To safeguard the nation’s energy independence and accelerate clean grid transitions, the U.S. Department of Energy (DOE) has announced a massive $17.5 billion loan initiative aimed at financing the manufacturing of nuclear reactor components. As reported by Mining.com Coverage, the funding targets critical vulnerabilities in the specialized, highly concentrated upstream supply chain, which has historically plagued large-scale energy projects with severe delays. By providing low-cost capital to domestic fabricators of heavy forgings, coolant pumps, and control systems, the initiative seeks to establish a resilient, highly localized manufacturing base. For supply chain managers within the industrial and utility sectors, this federal backing—signified by Westinghouse’s secured allocations outlined in the Cravath Legal Announcement—signals a major push to de-risk high-consequence procurement, shifting reliance away from bottlenecked foreign suppliers.

Beyond Software: Why the Future of TMS is an Operating Model

The traditional software model for Transportation Management Systems (TMS), in which shippers purchase a system of record solely to execute tenders, routing guides, and audits internally, is rapidly shifting. Shippers are increasingly looking beyond basic software features to invest in entire transportation operating models. This evolution reflects a growing operational reality: deploying complex software does not automatically generate logistics excellence, particularly when an organization lacks internal process maturity, a robust carrier strategy, or real-time exception-management capacity. To bridge this execution gap, industry categories are blurring as TMS software, managed transportation services, and digital freight brokerages converge. Modern buyers are shifting focus away from legacy functional checklists and toward integrated solutions that bundle technology with embedded capacity, workflow automation, and concrete outcome ownership.

Autonomous Tendering Is Coming for the Routing Guide

The traditional, static routing guide, long the central control mechanism for freight execution, is struggling to keep pace with highly volatile transportation markets. In response, modern logistics operations are transitioning toward autonomous tendering, redefining the routing guide from a fixed ladder of preferred carriers into a dynamic, policy-driven decision framework. Instead of manually cycling through a sequence of static, pre-negotiated carrier rankings that may be outdated or misaligned with current lane conditions, next-generation systems continuously evaluate live variables. By analyzing real-time capacity, historical acceptance rates, spot market alternatives, service risk, and facility constraints, these platforms can determine which carrier is most likely to deliver the optimal outcome under current conditions. This evolution does not eliminate contract rates or human oversight; rather, it establishes automated guardrails that operationalize procurement expertise at scale, ensuring logistics decisions are optimized for real-world execution rather than historical assumptions.

The post Supply Chain and Logistics News Weekly Round Up June 22nd-26th 2026 appeared first on Logistics Viewpoints.

Non classé

Carbon Is Becoming a Routing Constraint, Not Just a Reporting Metric

Published

1 jour agoon

26 juin 2026By

For many transportation organizations, sustainability reporting has historically been a retrospective exercise. Freight moved through the network, emissions were calculated after the fact, and the results were used for corporate reporting, customer disclosure, or ESG documentation.

That model is changing.

Transportation emissions are beginning to move from the reporting layer into the decision layer. As shippers face growing pressure from customers, regulators, investors, and internal sustainability commitments, carbon data will increasingly influence mode selection, routing, carrier choice, consolidation, and service tradeoffs.

Download the TMS Market Research Executive Summary for a strategic view of how transportation management systems are evolving to support cost, service, and sustainability decisions.

The important shift is this: carbon is becoming a transportation constraint, not just a reporting metric.

From After-the-Fact Measurement to Operational Decision-Making

Most transportation emissions programs began with measurement. Companies needed to estimate the carbon impact of freight activity across modes, lanes, carriers, and regions. That required better data on shipment distance, weight, equipment type, fuel usage, mode, and carrier activity.

Measurement was a necessary first step. But measurement alone does not change operations.

The next phase is embedding emissions data into transportation planning and execution. A TMS that calculates emissions after the shipment is complete provides reporting value. A TMS that uses emissions during planning provides decision value.

That difference matters.

If a transportation planner can compare cost, service, capacity, and carbon before selecting a routing option, sustainability becomes operational. It becomes part of the same tradeoff structure that already governs freight decisions.

The Transportation Tradeoff Is Getting More Complex

Transportation has always involved tradeoffs. Shippers balance cost, service, speed, reliability, capacity, and customer expectations. Carbon adds another variable to an already complex decision environment.

A lower-emissions option may cost more, take longer, require consolidation, shift freight from truckload to intermodal, or require a different carrier. It may reduce flexibility or conflict with customer delivery expectations. This is why sustainability in transportation is difficult. Most companies support the concept until it creates operational compromise.

The TMS will increasingly become the place where those compromises are made visible. Instead of treating carbon as a number calculated after the shipment is complete, the system will need to show how emissions compare against cost, service, capacity, and customer commitments before the transportation decision is made.

Carbon Data Must Be Decision-Grade

For emissions to become a routing constraint, the data must be good enough to support operational decisions. High-level estimates may be acceptable for annual reporting, but they are often insufficient for execution-level planning.

Transportation teams need emissions data that is reasonably accurate by lane, mode, carrier, shipment profile, and equipment type. They also need consistent methodology. If the data is not trusted, planners will ignore it.

This creates a new requirement for TMS platforms: sustainability logic must be explainable. Users need to understand why one option is estimated to produce lower emissions than another. They also need to know whether the difference is material enough to influence the decision.

A system that simply displays a carbon number without context will have limited impact.

The Role of TMS in Sustainable Transportation

The TMS is naturally positioned to operationalize transportation sustainability because it already manages many of the relevant decisions. Mode selection, load consolidation, routing, carrier assignment, pool distribution, appointment planning, backhaul opportunities, empty miles reduction, expedite avoidance, and service-level tradeoffs all influence emissions performance.

Many of the best sustainability improvements in freight are also efficiency improvements. Better consolidation, fewer empty miles, improved routing, and reduced expedites can lower both cost and emissions. But not every sustainability decision pays for itself. Some will require explicit prioritization. That is where TMS configuration and governance become important.

A shipper may set different emissions rules by customer, product, region, business unit, or service level. For example, the system may recommend lower-emissions options when cost and service differences fall within an acceptable tolerance. It may flag high-emissions shipments for review, prioritize intermodal on certain lanes, or calculate the emissions impact of premium freight. This turns sustainability from a corporate aspiration into an operating policy.

The Coming Tension Between Cost, Service, and Carbon

The most interesting market development will not be the ability to calculate emissions. It will be the willingness to act on that information.

If the TMS recommends a lower-emissions route that costs the same and meets the same delivery window, the decision is easy. The harder cases are where sustainability creates tradeoffs. A lower-emissions option may cost more, add a day to transit, require greater planning discipline from the customer, reduce delivery flexibility, or improve corporate emissions performance while increasing local operating complexity.

These questions cannot be answered by software alone. They require policy decisions. The TMS can expose the tradeoff, recommend options, and enforce rules. But leadership must decide how much carbon matters relative to cost and service.

Why This Matters for Buyers

Shippers evaluating transportation technology should treat emissions capabilities as more than a reporting module. The important question is whether carbon can be used inside the planning and execution workflow.

A strong TMS should estimate emissions before shipment execution, compare cost, service, and carbon across routing options, support emissions rules by lane, customer, product, or mode, and help planners evaluate consolidation and mode-shift scenarios. It should also connect emissions performance to carrier scorecards and provide enough transparency for sustainability metrics to be audited and explained.

These capabilities distinguish basic carbon reporting from transportation sustainability management. The value is not simply knowing what emissions were last quarter. The value is understanding which operational changes can reduce emissions in the next planning cycle, the next procurement event, or the next shipment decision.

Sustainability Will Become Part of Transportation Optimization

Carbon will not replace cost or service as the dominant transportation decision factor. Freight still has to move reliably and economically. But carbon will increasingly become part of the optimization model.

That is the real shift.

Sustainability reporting looks backward. Transportation optimization looks forward. The market is moving from one to the other.

The winners will be shippers that use emissions data not merely to explain what happened, but to improve what happens next.

Carbon is becoming a routing constraint. The TMS will be where that constraint becomes operational.

Download the TMS Market Research Executive Summary for a strategic view of how carbon, routing, and transportation decision intelligence are becoming part of the modern TMS market.

The post Carbon Is Becoming a Routing Constraint, Not Just a Reporting Metric appeared first on Logistics Viewpoints.

How Supply Chain Technology Providers Can Build Market Visibility with Research, Webinars, Podcasts, and Thought Leadership

Supply Chain and Logistics News Weekly Round Up June 22nd-26th 2026

Carbon Is Becoming a Routing Constraint, Not Just a Reporting Metric

Why Sulfuric Acid Is Emerging as a Supply Chain Constraint in Copper

Walmart and the New Supply Chain Reality: AI, Automation, and Resilience

Container rates starting to spike on peak season rush – June 2, 2026 Update

Trending

-

Non classé2 mois ago

Non classé2 mois agoWhy Sulfuric Acid Is Emerging as a Supply Chain Constraint in Copper

-

Non classé1 an ago

Non classé1 an agoWalmart and the New Supply Chain Reality: AI, Automation, and Resilience

- Non classé4 semaines ago

Container rates starting to spike on peak season rush – June 2, 2026 Update

- Non classé11 mois ago

13 Books Logistics And Supply Chain Experts Need To Read

- Non classé8 mois ago

Ex-Asia ocean rates climb on GRIs, despite slowing demand – October 22, 2025 Update

- Non classé5 mois ago

Container Shipping Overcapacity & Rate Outlook 2026

-

Non classé1 an ago

Non classé1 an agoAmazon and the Shift to AI-Driven Supply Chain Planning

- Non classé4 mois ago

Ocean rates ease as LNY begins; US port call fees again? – February 17, 2026 Update