Non classé

Top Supply Chain Risks to Prepare for in 2025

Published

2 ans agoon

By

This is the time of year when analysts get bombarded with pitches from PR firms. The pitches share a “sneak peek” of the predictions that a CEO at a solutions company is making and then asks the journalist if they want to interview the CEO. These predictions mostly seem obvious.

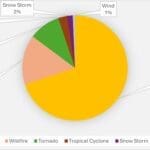

I got a pitch from the PR firm representing Everstream Analytics that was different. Everstream Analytics is sitting on a vast trove of risk data. The company applies AI and other analytics to this data to provide supply chain risk analytics and insights to its clients. In short, what makes them different is that they can quantify and thus prioritize supply chain risks.

Their 2025 outlook identifies the five most likely supply chain events that will impact supply chain operations this year. Each event is assigned a risk score.

Drowning in Climate Change

This is the top risk identified by Everstream. They apply a risk score of 90% here. “Flooding has become so volatile that even nations with the most sophisticated weather warning systems and infrastructure are caught off guard by the ferocity and speed of sudden flash flood events. Companies will be upended by even more frequent small-scale events and larger-scale storms like Hurricane Helene’s unexpected and extensive destruction across several states in the U.S. Appalachia region in 2024.”

The company points out that forecasted rainfall totals for Helene were very accurate one week in advance of the flood that devasted the Blue Ridge mountain region of North Carolina. “But nobody in that region had ever experienced or even expected that amount of rainfall in such a brief period. The existing infrastructure (bridges, roads, rails) was built in the past and was insufficient to handle these copious rainfall totals. The damage impacted more than 50 electronics, automotive, and aerospace manufacturers, plus general machinery and materials processors, and medical device and health care companies.”

Climate change is causing more frequent and intense extreme weather events around the world. In 2024, flooding events contributed to 70% of the weather disruptions covered by Everstream Analytics.

So, what can companies do about this risk? They recommend looking at key company-owned facilities and those run by key partners and suppliers. The “evaluation should include a review of area infrastructure, egress routes, and waterways. Pay attention to applied meteorology forecasts as far in advance as possible and take flood warnings particularly seriously. Prepare for the worst and react aggressively.”

Geopolitical Instability with Increased Tariff Risk

Everstream applies a score of 80% to this risk. “International political and economic relations are destabilizing, caused by political upheaval, ongoing skirmishes, and full-scale wars. In 2025, it will be impossible to avoid conflict and its impact on sourcing, manufacturing, and logistics.”

The report cites intensified political turmoil in the Middle East, including the Israeli-Hamas war and its spillover, the Syrian civil war, and continuous Houthi attacks on Red Sea vessels. “Even if the traffic along the Suez Canal route returns to full throttle in 2025, this shift would cause weeklong processing delays, container backlogs, and a spike in congestion at many European seaports due to the sudden increase in cargo volume.”

In Ukraine, Russian forces now occupy around 20% of the country. Additional support from Western allies looks less likely. It is likely Russia will be able to destabilize Ukraine’s remaining manufacturing and trade activities and that further strain between Europe and Russia will result.

In Asia-Pacific, China believes Taiwan rightfully belongs to them. This has led to the souring of cross-strait relations between China and Taiwan as Taiwan exhibits more political independence. “A full-scale invasion seems unlikely.” This may be overly optimistic. However, the report summarizes the military drills around Taiwan in recent years and comments that “more or bigger Chinese military exercises could disrupt transportation through significant seaports and airports in the region. Nearly a third of all global trade – and 40% of all globally traded petroleum products – flows through sea lanes in the region.

Meanwhile, tariff increases always affect global trade flows. President Trump has proposed tariff increases, including a global baseline tariff of 10–20%, a 60% tariff on Chinese imports, and a 100% tariff on goods from de-dollarizing countries. De-dollarization is an effort by several countries to reduce the role of the U.S. dollar in international trade. Countries like Russia, India, China, among others, are seeking to set up trade channels using currencies other than the dollar.

Everstream’s report did not mention Mexican or Canadian tariffs. An increase in the flows between China and Mexico of assembled products, and materials and components produced in China has occurred. This has been described as a “back door” into the U.S. to avoid Trump and Biden administration tariffs. Trump’s negotiations with Mexico to close the back door could heighten the impact of new tariffs on China.

The automotive, semiconductor, and manufacturing industries are at risk due to potential tariffs on solar wafers, polysilicon, steel/aluminum imports, and the closure of the back door to Mexico. Additionally, tariffs on Chinese goods could lead to retaliatory measures, affecting U.S. companies operating in China. This would primarily affect U.S. agricultural exports and finished goods.

The key strategy, according to Everstream, is to understand the multi-tier supply sources by country so that a company can make sourcing adjustments when an event occurs. If a company can do this more quickly than its competitors, that leads to a competitive advantage.

More Back Doors for Cybercrime

Everstream assigns this risk a score of 75%. “While a company’s cybersecurity front doors may be double-bolted, but there are more unlocked back doors than ever available to increasingly sophisticated attackers. In 2025, cyberattacks will primarily arrive via sub-tier supply chains, where criminals can more easily exploit common programming errors and vulnerabilities. They can then leapfrog into top-tier corporations via phishing, software connection links, or other methods.”

Cencora, a sub-tier pharmaceutical supplier, had a security breach in the early spring of 2024. At least 11 global pharmaceutical companies linked this breach to their later ransomware and phishing attacks. Everstream’s data document 471 attacks in 2024. The data shows that cyberattacks were particularly common in the electronics, logistics, and consumer goods industries.

Larry O’Brien, a vice president at ARC Advisory Group, says that an European Union regulation known as Network and Information Systems Directive 2 provides a good framework for companies to follow to bolster their supply chain cybersecurity capabilities. While NIS 2 is an EU regulatory framework, NIS 2 applies to companies headquartered outside the EU if they provide services within the EU. “Adopting a risk management framework for cybersecurity is something that all manufacturers should be doing,” Mr. O’Brien points out. “As with any regulatory framework, NIS 2 tells you what needs to be done, not always how to do it.”

Rare Metals and Minerals on Lockdown

The score assigned to this class of risks is 65%. “Countries and companies alike are recognizing global mineral scarcity coupled with increasing demand, and both are responding by locking up supplies.” Between rising regulations, new tariffs, and long-term or exclusive contracts, rare minerals and metals will be harder and more expensive to obtain.

“Within a politically charged atmosphere between the West and the major commodity producers—China and Russia—companies will face new tariffs and sanctions on critical metals. Governments are placing renewed emphasis on the negative environmental and social impacts of mining, which will present challenges for metal producers over the coming year.”

But, China is not the only nation with proposed or enacted commodity restrictions. “Political tensions over the Russia-Ukraine war led to restrictions on Russian metal imports by the U.S. and the UK. Additionally, security concerns and allegations of industry product dumping led many countries to enact measures against Chinese metal imports.”

As concerns mount surrounding critical commodities, companies are increasingly turning to direct mineral purchasing agreements with mines. However, when a nation supplies an overwhelming majority of a mineral based on mining or processing, direct agreements with mines may have limited value. Graphite, for example, is a core raw material for producing Lithium batteries which are core to the electronic vehicle market. 80% of the world’s graphite is produced in China.

Crackdown on Forced Labor

No nation’s enforcement of any ESG issue comes close to the US Customs and Border Protection Agency’s enforcement of the Uyghur Forced Labor Protection Act. $3.7 billion in shipments have been detained at the border based on enforcement of this act. In some cases, the shipments are eventually cleared, but only after supply chains were disrupted and demurrage charges accrued. But a significant proportion of shipments were never allowed entry into the US.

What gives the US act teeth is that “the ‘rebuttable presumption’ part of UFLPA is truly unique. Anything coming out of Xinjiang is presumed to have used forced labor unless an importer can prove the negative. There is also a lack of a de minimis exception; this means that even an insignificant input of product produced in whole or in part with forced labor could result in enforcement action.

While the UFLPA is the most stringent, other nations and regions have also enacted legislation. These include the EU’s Corporate Sustainability Due Diligence Directive (CS3D) and regulation on Prohibiting Products made with Forced Labor (FLR); Mexico’s Forced Labor Regulation; and Canada’s Fighting Against Forced and Child Labour in Supply Chains Act.

While legislation has pushed many companies to find alternative suppliers in other low-income countries, many emerging economies do not have adequate laws or enforcement mechanisms. This is particularly true when sub-tier suppliers employ migrant labor.

The technology exists to detect whether a company’s supply chain includes sub-tier suppliers based in the Uighur region of China. This technology is not flawless, there can be false positives and misses. Nevertheless, it is a powerful tool to prevent shipments from being detained based on UFLPA.

However, finding bad actors among sub-tier suppliers in other parts of the world is still difficult. Everstream points out that the food industry is a particular source of concern. Vanilla, palm oil, cocoa, and soy – produced in Madagascar, Indonesia, Cote d’Ivoire, Ghana, and Nigeria – have frequently accrued violations and allegations based on child labor or forced labor issues.

The post Top Supply Chain Risks to Prepare for in 2025 appeared first on Logistics Viewpoints.

You may like

Non classé

Transpac peak may stretch on even as Asia – Europe ocean cools – August 6, 2026 Update

Published

1 jour agoon

7 août 2026By

Weekly highlights

Ocean rates – Freightos Baltic Index

Asia-US West Coast prices (FBX01 Weekly) decreased 1%.

Asia-US East Coast prices (FBX03 Weekly) stayed level.

Asia-N. Europe prices (FBX11 Weekly) decreased 1%.

Asia-Mediterranean prices (FBX13 Weekly) decreased 2%.

Air rates – Freightos Air Index

China – N. America weekly prices decreased 2%.

China – N. Europe weekly prices increased 5%.

N. Europe – N. America weekly prices decreased 2%.

Analysis

After weeks of violent escalations in US-Iran tensions surrounding the status of the Strait of Hormuz, Iran and Oman may soon announce a bilateral agreement to reopen the waterway.

The deal would open the Hormuz – without tolls or fees on transiting vessels – for sixty days, with ships entering the Persian Gulf in coordination with Iran along the northern lane, and exiting in coordination with Oman via the southern lane.

Join 70,000+ Supply Chain Experts Who Never Miss an Issue!

Start your week with the industry insights others miss.

« * » indicates required fields

Consent*

Following the failed June Memorandum of Understanding, this agreement – which may not go into effect immediately and may be contingent on the US removing its blockade of Iranian ships – will attempt to create enough stability for renewed US-Iran negotiations toward an end to the conflict. But, by validating Iranian control over the strait, the deal would mark a significant de facto concession to Iran – despite serious earlier opposition from both the US and multiple Gulf states among others – and change to the pre-war status quo.

If the strait is reopened, the rebound in traffic will be gradual and, with the main central channel still closed due to Iranian mines, may not recover to normal levels under the new arrangement.

For the container market, more vessels will exit than enter at first, with long haul ships likely to stay away until carriers are confident this ceasefire is stable. The reopening should also ease some of the strain on the landbridge alternatives in the region, though carriers may be hesitant to send feeder vessels into the Gulf at first as well. If the reopening goes smoothly and contributes to progress in US-Iran negotiations – and if developments include a Saudi Arabia – Houthi deescalation – carriers may resume earlier cautious moves back toward Red Sea transits as well.

The biggest impact of a Strait of Hormuz reopening for logistics would be on oil prices. Crude prices had eased back to pre-war levels when the ceasefire took hold in late June and early July, but then shot up 35% and past $90 a barrel by late July. The recent de-escalation has prices down 18% since late July – only 10% above the baseline – and a reopening should push prices lower. Bunker prices that climbed 16% since early July have leveled off over the past two

weeks but are still 50% higher than before the start of the war. The resumption of crude flows should start putting downward pressure on refined products like bunker and jet fuel too, though the effect may not be immediate.

Even if oil prices ease in the near term, peak season supply-demand dynamics – not fuel costs – are the major drivers of container spot rate behavior for now.

Ocean peak season started early this year, with surging demand consistently pushing rates up across the major east – west lanes from late May through early July. BAF increases and manufacturer price hikes set for Q3 drove some of the frontloading, with some US shippers pulling peak season orders forward ahead of a late July tariff deadline.

But since early July – and despite planned GRIs and PSSs including for August 1st – rates on most of these lanes have eased or at least leveled off, suggesting that the frontloading-driven peak season rush was cooling earlier than usual too.

Asia – Europe rates decreased slightly last week, but dipped by another $500/FEU so far this week. Asia – N. Europe prices of about $5,000/FEU are down 14% from their July peak, with Asia – Mediterranean rates at $6,000/FEU, 16% below the July peak and about back to mid-June levels. Some carriers have additional significant increases slated for mid-August, but rate behavior over the last few weeks and reports of easing demand and increases in blanked sailings may make rate increases unlikely.

On the transpacific, East Coast rates have been stable at their peak level of about $9,000/FEU since early July. West Coast rates reached a peak of more than $7,500/FEU in early July and through last week had eased about 20% to around $6,000/FEU.

But West Coast daily rates so far this week have jumped back above $7,000/FEU on August 1st GRIs. NRF US ocean import volume projections last month estimated that demand in August would be well below July levels. But steady East Coast rates together with some forwarder reports of surprisingly strong demand and this recent West Coast rate bump may indicate that peak season strength is lasting longer than anticipated on the transpacific.

If these rate increases stick – or climb even higher on August 1st GRIs of $2,000 – $3,000/FEU – experts are offering multiple reasons for why peak demand may be holding up past the frontloading deadlines, including unexpectedly low inventory levels and stronger than anticipated consumer demand.

Another reason may be that the July 24th tariff deadline did not result in sharp tariff hikes. Many US shippers were frontloading peak season volumes ahead of the Section 122, 10% global tariff July 24th expiration date out of concern that duties could be higher soon after. Instead, Section 122 tariffs were immediately replaced by Section 301 tariffs on more than sixty trade partners – aimed at curbing forced labor imports – of 10% to 12.5% or about even with the expiring duties.

The USTR recently stated that its 301 investigation into excess manufacturing capacity by sixteen of the largest US trading partners is nearing completion. These tariffs could raise duty levels back to those set using IEEPA. But even once the USTR shares its findings, it will take several weeks before the president could implement the recommendations. This gap may be extending tariff frontloading by some shippers, likewise contributing to a longer than expected transpacific peak.

Finally, for all lanes – including Asia – Europe trades where consensus is that demand is cooling – rates may be facing upward pressure from supply side constraints as well, since two major typhoons struck Far East ports over the last few weeks. Typhoon Noul shut down ports in southern China in late July as regional hubs were still recovering from a mid-month storm. Some carriers are now skipping Shanghai port calls as congestion remains severe there, with multi-day delays also reported in Ningbo, Shenzhen and Hong Kong.

In air cargo, some carriers have announced increases in fuel surcharges for August as jet fuel prices that have leveled off in the last couple weeks remain 33% higher than a month ago. For now though, global prices have continued their slow season slide with the Freightos Air Index global benchmark down 8% compared to the end of June.

China – US rates eased 2% last week to $5.67/kg. And though China – Europe prices climbed 5% to $4.02/kg last week, they remain more than 10% lower than a month ago, as the end of de minimis in the EU has led to lower volumes and rates on this lane even as carriers shift capacity to higher demand origins like Taiwan, where AI hardware is keeping volumes elevated.

Freightos Terminal: Real-time pricing dashboards to benchmark rates and track market trends.

Procure: Streamlined procurement and cost savings with digital rate management and automated workflows.

Rate, Book, & Manage: Real-time rate comparison, instant booking, and easy tracking at every shipment stage.

The post Transpac peak may stretch on even as Asia – Europe ocean cools – August 6, 2026 Update appeared first on Freightos.

Non classé

Supply Chain and Logistics News Round Up of the Week (August 4th-7th 2026)

Published

1 jour agoon

7 août 2026By

The global supply chain landscape is transforming before our eyes this week, marked by a dual focus on radical simplification and high-frontier innovation. While automotive giants like BMW and Ford are aggressively stripping out complexity to safeguard margins in an era of tightening trade rules, aerospace leaders SpaceX and NVIDIA are looking skyward, positioning AI compute payloads in orbit to redefine real-time logistics visibility. Yet, this push for efficiency is unfolding against a backdrop of intense regulatory volatility, as evidenced by a massive 25-state legal challenge to new Section 301 tariffs. Amidst these shifting currents, PepsiCo’s latest economic data provides a stabilizing perspective, demonstrating how deeply embedded sustainability practices are no longer just ESG milestones, but essential drivers of long-term network resilience and growth.

The Biggest Supply Chain Stories of the Week:

European Trade Rules and Margin Squeezes Force BMW into Deep Restructuring

Automotive leaders in Europe are confronting structural margin compression alongside tightening regional content rules, as highlighted in a recent analysis of BMW’s European automotive supply chain restructuring. Following a sharp drop in second-quarter deliveries in China and a reduction in projected 2026 automotive margins, operations are pivoting toward flatter administrative structures, reduced model variations, and streamlined engineering processes. Concurrently, European policy proposals establishing high “Made in Europe” local-value thresholds are transforming vehicle origin verification into a complex multi-tier tracking requirement. For tier-one and tier-two component suppliers, this regulatory transition demands granular visibility into raw materials, battery cell origins, and software value addition across global production networks.

2SpaceX and NVIDIA Collaborate to Position AI Compute Payloads in Orbit

In a deployment aimed at processing complex global data near its physical source, aerospace and technology developers are partnering to build orbital compute infrastructure. Detailed in an evaluation of SpaceX and NVIDIA’s orbital AI infrastructure initiative, future satellite constellations are planned to carry standardized hardware capable of executing machine learning models directly in space. By filtering atmospheric imagery, ocean vessel positioning, and infrastructure data before ground transmission, orbital edge computing aims to reduce bandwidth bottlenecks and accelerate signal processing. For supply chain visibility networks and risk-management platforms, this architecture points toward automated exception detection where satellite nodes directly output machine-readable event alerts to ground-based transportation management platforms.

Ford Cuts Product Complexity to Drive Low-Cost Vehicle Economics

Automotive manufacturing models are undergoing significant simplification to lower capital intensity and improve production economics. As examined in a strategic review of Ford’s platform simplification and manufacturing model, major vehicle OEMs are paring down low-margin derivative models to concentrate volume around a smaller selection of core platforms. By decreasing overall component counts, minimizing assembly touches, and standardizing structural chassis designs, manufacturers aim to reduce inbound freight complexity and eliminate points of failure along the assembly line. This shift integrates mass customization into the customer ordering interface rather than the assembly stage, allowing logistics operators to streamline tier-one supplier scheduling and maintain lower safety stock cushions.

25 States Sue Trump Over Section 301 Forced-Labor Tariffs

A coalition of 25 states has filed a lawsuit in the U.S. Court of International Trade challenging the Trump administration’s newly imposed Section 301 tariffs on 60 trading partners—including China, the EU, Canada, and Mexico—which levy duties of 10% to 12.5% under the explicit banner of combating forced labor. The suit argues that forced labor is a pretextual workaround to replace broad tariffs previously struck down by the Supreme Court under the International Emergency Economic Powers Act (IEEPA), highlighting that the U.S. Trade Representative failed to link tariff rates to actual forced-labor prevalence, ignored public testimony, and established no remedial path or off-ramp for compliant nations. Coming on the heels of similar litigation from commercial importers, this legal battle underscores continuing trade policy volatility, leaving procurement and logistics operations to navigate ongoing cost uncertainty, administrative stays, and potential duty refund scenarios.

PepsiCo Links Sustainable Practices to Supply Chain Growth

A new economic impact report from PepsiCo, verified by Oxford Economics, underscores how embedding sustainable practices into upstream operations drives macro-level supply chain resilience and broader economic stability. According to the analysis, the food and beverage giant supported nearly 440,000 U.S. jobs in 2024—adding roughly two external multiplier jobs across agriculture, logistics, and packaging for every direct employee—while contributing $64.88 billion to U.S. GDP. Beyond direct employment metrics, the report explicitly ties these workforce and operational nodes to long-term ESG milestones, highlighting how expanding regenerative agriculture across 4.7 million acres and reaching 100% water replenishment in high-risk watersheds safeguard essential raw commodity inputs against climate disruption. For enterprise supply chain strategists, PepsiCo’s data presents a clear business case for natural resource stewardship, proving that localized sustainability investments are vital risk mitigation mechanisms that secure supplier networks, stabilize tier-one communities, and protect core manufacturing throughput.

Song of the Week:

The post Supply Chain and Logistics News Round Up of the Week (August 4th-7th 2026) appeared first on Logistics Viewpoints.

Non classé

BMW’s Job Cuts Reveal the Real Battle Over Europe’s Automotive Supply Chain

Published

2 jours agoon

6 août 2026By

BMW has spent the past several years looking like the most composed member of Germany’s increasingly unsettled automotive industry.

Volkswagen has been trying to shrink a cost structure built for a larger European market. Porsche has struggled with falling demand in China. Mercedes-Benz has been cutting costs and reconsidering the breadth of its vehicle portfolio.

BMW appeared to have given itself more room to maneuver.

It continued investing in electric vehicles without committing its entire future to a single propulsion technology. Its factories retained the flexibility to build combustion, plug-in hybrid, and electric models. Its premium positioning also offered some protection from the price competition consuming the lower end of the market.

That strategy has not failed. But it has not insulated BMW from the forces now reshaping the European automotive industry.

BMW said in late July that it would eliminate several thousand positions in Germany by the end of 2027 through a voluntary severance program. The cuts are aimed at administrative and development functions, not production workers. Reuters, citing a person familiar with the plan, reported that BMW’s global workforce could eventually decline by roughly 8,000 positions. BMW has not publicly confirmed that figure.

The distinction matters.

This is not simply another automaker cutting factory employment because demand weakened. BMW is taking a harder look at how the company is managed, how decisions move through the organization, and how much overhead is required to develop and sell a vehicle.

At nearly the same time, France, Germany, and the European Commission are moving toward a more deliberate effort to keep automotive production and component value inside Europe.

The two developments belong together.

BMW is trying to become leaner and faster. Europe is preparing to make automotive sourcing more regional, more traceable, and more closely tied to public policy.

The first effort may simplify BMW. The second could make its supply chain considerably more complicated.

BMW’s Margins Leave Little Room for Delay

BMW’s second-quarter results explain why management is prepared to revisit structures that once appeared permanent.

Group profit before tax fell 35.1% from the previous year to €1.697 billion. Revenue declined 7.9% to €31.259 billion. Within the automotive segment, earnings before interest and taxes fell 60.7% to €629 million. The automotive operating margin dropped from 5.4% to 2.3%.

BMW attributed the pressure to lower volumes, intense competition in China, currency movements, higher depreciation, commodity costs, and additional U.S. tariffs. Tariffs alone reduced the automotive margin by approximately 1.25 percentage points during the second quarter and first half.

The company has already been cutting spending. Selling and administrative expenses in the automotive business fell 8.3% during the quarter. But those reductions were not enough to offset the deterioration in the market.

China remains the most immediate problem.

BMW Group deliveries in China fell 30.2% during the second quarter, from 168,959 vehicles to 117,927. Deliveries were down 20.4% for the first half. Global second-quarter deliveries declined 4.9%, despite growth in Europe and the United States.

China once provided German premium automakers with a powerful source of volume, profit, and confidence. Those earnings helped finance large engineering organizations, broad vehicle portfolios, and the enormous cost of developing the next generation of vehicles.

That economic engine is becoming less dependable.

Chinese automakers are no longer simply lower-cost competitors. They are developing new vehicles quickly, integrating software effectively, and competing most aggressively in the electric-vehicle segments where much of the industry’s investment is now concentrated.

BMW has reduced its expected 2026 automotive margin from 4%–6% to 1%–3%. It now expects deliveries to decline slightly and group profit before tax to fall significantly from the previous year.

Those numbers turn the discussion from incremental improvement to structural change.

The Next Restructuring Will Reach the Office

BMW’s decision to focus voluntary departures on administration and development says a great deal about where management believes the company has become too heavy.

Automotive complexity accumulated over decades. New regions, brands, technologies, regulations, and vehicle programs created new processes. Those processes created committees, specialists, interfaces, and layers of management.

That structure was easier to support when margins were higher and China was growing. It becomes much harder to justify when an automaker must simultaneously fund combustion engines, plug-in hybrids, battery-electric vehicles, software platforms, batteries, and autonomous-driving systems.

BMW’s new CEO, Milan Nedeljkovic, has said the company will revisit processes and structures that were previously considered untouchable. The review will extend across sales, procurement, production, and development. BMW also plans to reduce some model variants where demand no longer justifies the complexity.

That may matter more than the final number of job cuts.

A company can remove thousands of positions and still leave the underlying work untouched. The remaining employees simply inherit the same reports, approvals, meetings, and handoffs.

BMW’s real challenge is to remove work from the system.

That may mean fewer model combinations, fewer approval layers, tighter engineering priorities, and a more direct connection between product decisions and supplier execution.

Artificial intelligence will have a role in document-heavy areas such as procurement, engineering support, finance, and compliance. But the technology is not the central story.

The real test is whether BMW uses it to eliminate steps and shorten decision cycles, or merely asks a smaller workforce to operate the same complicated organization.

Germany’s Supplier Base Faces the Harder Transition

BMW’s restructuring will attract attention because of the company’s size. The more severe adjustment may occur among suppliers.

The German Association of the Automotive Industry estimates that the country lost roughly 100,000 automotive jobs between 2019 and 2025. It projects that another 125,000 could disappear by 2035 under current conditions.

Suppliers are caught between two technology systems.

They must continue supporting combustion vehicles that still generate substantial volume and cash flow. At the same time, they must invest in electric drivetrains, battery systems, power electronics, sensors, software, and thermal management.

The old business is expected to decline. The new business often lacks the scale or margins to replace it.

Automakers also continue pushing suppliers for cost reductions while those suppliers face higher European energy, labor, financing, and regulatory costs.

This is why European suppliers are pressing for a meaningful definition of “Made in Europe.”

Their concern is not simply where final assembly occurs. A vehicle can be assembled in Europe while much of its battery, electronics, materials, software, and component value comes from elsewhere.

Europe retains the assembly jobs but gradually loses the industrial capabilities that determine where engineering expertise, intellectual property, and future investment reside.

“Made in Europe” Becomes a Supply-Chain Rule

The European Commission’s proposed Industrial Accelerator Act is an attempt to reverse that drift.

Introduced in March, the proposal would increase demand for European-made, low-carbon industrial products and strengthen capacity in strategic sectors. For the automotive industry, it would connect selected public support and procurement programs to European assembly, regional content, and critical-component requirements.

The proposal has not yet completed the EU legislative process.

According to the framework described by the European automotive supplier association CLEPA, a qualifying vehicle would need to be assembled in the EU and meet a 70% regional-content threshold. A separate 50% threshold for designated critical components would take effect three years after the final regulation is published.

The political logic is straightforward. Europe does not want public money intended to support European industry flowing primarily into imported batteries, electronics, and other technologies.

The supply-chain implications are much less simple.

A 70% threshold turns the nationality of a vehicle into a data problem.

Automakers will need to know not only where final assembly occurred, but where the value inside the vehicle originated. That may require tracing battery cells, power electronics, semiconductors, magnets, software, castings, and raw-material processing across multiple supplier tiers.

Most automakers have strong visibility into tier-one suppliers. Visibility further upstream is far less consistent.

A battery pack may be assembled in Europe using cells produced elsewhere, materials processed in another country, and electronic controls from a third. A semiconductor may be designed in Europe, fabricated in Asia, and packaged in another region.

Regional-content rules will turn those relationships into eligibility decisions.

Procurement teams will have to consider whether a sourcing choice moves a vehicle above or below the threshold and whether that affects access to public incentives or government purchasing programs.

The least expensive component may no longer produce the lowest total cost.

Europe Can Buy Time, Not Competitiveness

There is a legitimate case for protecting critical European industrial capabilities.

China has used coordinated investment, financing, infrastructure, procurement, and industrial policy to build strong positions in batteries, electric vehicles, critical-material processing, and solar technology. The United States has also become more willing to connect public incentives to domestic production.

Europe is responding to a world in which its competitors are already managing industrial outcomes.

But regional-content rules cannot solve BMW’s core operating problems.

They cannot shorten vehicle-development programs, improve software, eliminate unnecessary approvals, restore Chinese demand, or guarantee that a European supplier is globally competitive.

Industrial policy may create time, demand, and investment incentives. BMW still has to use that time well.

That is the tension at the center of the story.

Europe is trying to preserve the automotive supply chain from the outside. BMW is trying to rebuild its competitiveness from the inside.

Both efforts may be necessary. Neither is sufficient on its own.

The future of Europe’s automotive industry will not be determined simply by how many vehicles are assembled in Munich, Stuttgart, Wolfsburg, or elsewhere in the EU.

The more important question is how much of the vehicle’s value is created there.

Europe could retain assembly plants while losing batteries, electronics, software, semiconductors, materials processing, and engineering. Cars would still leave European factories, but a smaller share of the economic and technological value would remain in Europe.

BMW’s cuts are therefore more than another automotive cost program. They are evidence that the next restructuring will extend through management, development, procurement, supplier networks, and the rules used to determine where a vehicle truly comes from.

Europe is preparing to defend its automotive industrial base.

BMW is preparing for the possibility that defense will only buy time.

The post BMW’s Job Cuts Reveal the Real Battle Over Europe’s Automotive Supply Chain appeared first on Logistics Viewpoints.

Transpac peak may stretch on even as Asia – Europe ocean cools – August 6, 2026 Update

Supply Chain and Logistics News Round Up of the Week (August 4th-7th 2026)

BMW’s Job Cuts Reveal the Real Battle Over Europe’s Automotive Supply Chain

Container rates jump another $1k/FEU – but is demand peaking? – July 8, 2026 Update

Walmart and the New Supply Chain Reality: AI, Automation, and Resilience

Why Sulfuric Acid Is Emerging as a Supply Chain Constraint in Copper

Trending

- Non classé1 mois ago

Container rates jump another $1k/FEU – but is demand peaking? – July 8, 2026 Update

-

Non classé1 an ago

Non classé1 an agoWalmart and the New Supply Chain Reality: AI, Automation, and Resilience

-

Non classé4 mois ago

Non classé4 mois agoWhy Sulfuric Acid Is Emerging as a Supply Chain Constraint in Copper

- Non classé2 mois ago

Container rates starting to spike on peak season rush – June 2, 2026 Update

- Non classé12 mois ago

13 Books Logistics And Supply Chain Experts Need To Read

- Non classé10 mois ago

Ex-Asia ocean rates climb on GRIs, despite slowing demand – October 22, 2025 Update

- Non classé1 mois ago

LCL Shipping Cost Calculator: Calculate Air and Sea Shipping Freight Rates

- Non classé6 mois ago

Container Shipping Overcapacity & Rate Outlook 2026