Non classé

Federal Industrial Partnerships and Supply Chain Realignment Under the Trump Administration: Pharmaceuticals, Semiconductors, Critical Minerals, and Energy

Published

9 mois agoon

By

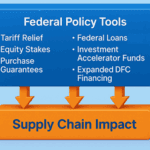

In the months leading up to the 2026 midterm elections, the Trump administration has launched a broad initiative to negotiate agreements with companies across as many as thirty industries. According to reporting from Reuters and other outlets, these deals involve a range of mechanisms, including tariff relief, equity stakes, revenue guarantees, and regulatory adjustments.

The purpose of the initiative, according to administration officials, is to strengthen U.S. national and economic security by encouraging companies to expand production domestically, reduce reliance on China, and ensure the availability of critical products.

For logistics and supply chain leaders, this represents a significant change in the relationship between government and industry. Federal agencies are no longer simply regulators or supporters of infrastructure. They are becoming active participants in corporate strategy, investment, and supply chain design.

Structure of the Deals

The administration’s approach is not uniform. Each agreement varies depending on the sector and company involved. Examples include:

Pharmaceuticals: Eli Lilly was asked to expand insulin production, Pfizer was pressed to increase output of its cancer and cholesterol drugs, and AstraZeneca was encouraged to establish a new U.S. headquarters. In exchange, companies have been offered tariff relief or regulatory flexibility.

Semiconductors: A portion of grants provided under the CHIPS Act has been converted into equity stakes, including a reported 10 percent stake in Intel.

Critical Minerals: The Department of Defense took a 15 percent stake in MP Materials, secured a floor price for future government purchases, and facilitated a $500 million supply agreement between MP Materials and Apple for rare earth magnets.

Energy: The Department of Energy has asked companies such as Lithium Americas for equity stakes in exchange for federal loans supporting domestic mining and battery production.

The unifying theme is the use of federal leverage, such as tariffs, financing programs, or regulatory approvals, to secure commitments from private companies that align with stated national security objectives.

Agencies as Dealmakers

What distinguishes this initiative is the scale of inter-agency involvement. The White House has described the approach as “whole of government.”

The Department of Health and Human Services is leading negotiations in pharmaceuticals.

The Department of Commerce, under Secretary Howard Lutnick, has overseen transactions in steel, semiconductors, and industrial manufacturing.

The Department of Energy is linking financing programs to equity arrangements in energy and mining.

The Pentagon has led negotiations with defense contractors and suppliers of critical minerals.

Senior officials, including White House Chief of Staff Susie Wiles and supply chain coordinator David Copley, are directly involved in negotiations. The presence of Wall Street dealmakers, such as Michael Grimes (formerly of Morgan Stanley) and David Shapiro (formerly of Wachtell, Lipton, Rosen & Katz), illustrates the administration’s transactional orientation.

Financing Mechanisms

The administration is using multiple sources of capital to finance these arrangements:

International Development Finance Corporation (DFC): Originally designed to support development projects abroad, the DFC has proposed expanding its budget authority from $60 billion to $250 billion. If approved by Congress, it would fund projects in infrastructure, energy, and critical supply chains within the U.S.

Investment Accelerator (Commerce Department): Seeded by $550 billion pledged by Japan as part of a bilateral trade agreement, this entity will direct capital into U.S. strategic sectors, serving as a replacement for an earlier proposal to establish a sovereign wealth fund.

Existing Programs: Agencies are repurposing funds from programs such as the CHIPS Act and Department of Energy loan guarantees, often converting grants into equity holdings.

Together, these mechanisms represent one of the largest coordinated federal interventions in U.S. industrial and supply chain development in recent decades.

Implications for Supply Chains

The administration’s policies carry several direct consequences for logistics and supply chain management.

1. Reshoring of Manufacturing

Many of the deals include explicit requirements for expanded U.S. production. This will increase demand for domestic transportation, warehousing, and distribution capacity. It also implies higher utilization of U.S. ports and intermodal corridors, as inputs shift from finished imports to raw materials and intermediate goods requiring processing inside the United States.

2. Critical Minerals and Energy Security

The focus on rare earths, lithium, and other inputs for advanced manufacturing indicates a restructuring of upstream supply chains. Logistics providers should expect increased flows from domestic mining regions, such as Nevada’s Thacker Pass lithium project, to processing and manufacturing centers. This represents a shift away from reliance on Asian supply hubs, particularly China.

3. Government as Stakeholder

Equity stakes and long-term purchase agreements create a different operating environment. Logistics providers serving these industries may find demand more stable due to government-backed contracts. However, these arrangements may also impose compliance requirements and reduce flexibility in adjusting supply networks.

4. Public-Private Coordination

Federal involvement in freight and industrial infrastructure financing could accelerate long-delayed projects. Rail expansion, port upgrades, and domestic warehouse capacity may benefit from this investment. Companies positioned to partner on these projects may see long-term opportunities.

Risks and Concerns

Several risks accompany this shift:

Policy Reversal: Executives have expressed concern that a future administration could unwind or renegotiate these deals. Supply chains built around government-backed agreements may face uncertainty if political priorities shift.

Equity Demands: Some companies are wary of ceding ownership stakes to the federal government. This creates hesitation in sectors where ownership control and investor confidence are sensitive.

Market Distortions: Critics argue that selecting which companies receive government support could disadvantage firms excluded from the arrangements, altering competitive dynamics within industries.

Implementation Capacity: The scale of proposed financing, particularly the expansion of the DFC, requires congressional approval and capable management. Delays or political opposition could slow execution.

Policy-to-Supply-Chain Impact Table

Policy Mechanism

Industry Example

Government Action

Supply Chain Impact

Tariff Relief

Pharmaceuticals (Pfizer, Eli Lilly)

Tariff exemptions in exchange for expanded U.S. production

Increases demand for domestic warehousing, distribution, and cold-chain logistics for added output

Equity Stakes

Intel (10% stake), MP Materials (15% stake)

Federal ownership through converted grants or Defense Production Act

Creates long-term stability in supply flows, but may add compliance requirements for logistics providers

Purchase Guarantees

MP Materials with Apple

Pentagon set floor prices, Apple committed to $500M supply contract

Locks in demand for rare earth shipments, increasing domestic transport flows from mining to manufacturing

Federal Loans Linked to Equity

Lithium Americas (DOE loan, 5–10% stake requested)

Loan support tied to partial government ownership

Supports new mining and battery projects, creating future logistics demand for raw materials and finished batteries

Investment Accelerator Funding

Commerce Department

$550B in financing, partly funded by Japan, allocated to U.S. manufacturing and freight infrastructure

Potential expansion of ports, intermodal rail, and distribution centers, reducing bottlenecks in supply chains

Expanded DFC Financing

Multiple critical industries

Proposed budget growth from $60B to $250B for U.S. supply chains and infrastructure

Large-scale capital for freight corridors, warehouses, and strategic materials, enabling reshoring of production

Case Examples

MP Materials

The rare earth mining company received federal backing through a 15 percent Pentagon stake, floor pricing commitments, and a supply agreement with Apple. This illustrates the administration’s template: equity participation, purchase guarantees, and private-sector co-investment.

Intel

The conversion of CHIPS Act funding into a 10 percent federal equity stake in Intel highlights the new approach to semiconductor supply chain security. By tying financial support to ownership, the government ensures both accountability and a direct role in strategic sectors.

Lithium Americas

A Department of Energy loan of $2.26 billion, paired with negotiations for a 5 to 10 percent federal equity stake, demonstrates how energy supply chains, particularly those tied to electric vehicles and batteries, are being secured through mixed financing and ownership arrangements.

Long-Term Outlook

The administration’s strategy marks a departure from the traditional U.S. model of private-sector–led industrial development. Instead, it resembles coordinated industrial policies pursued in other economies, though with American characteristics.

For supply chain professionals, this means that:

Government will play a larger role in shaping sourcing, production, and distribution decisions.

Access to federal financing and contracts will become a key factor in strategic planning.

Logistics infrastructure may receive substantial investment, creating new opportunities for providers.

Companies must assess political as well as market risks when designing long-term supply chains.

The Trump administration’s pre-midterm industrial deals reflect a significant realignment of government and industry roles in the United States. By leveraging tariffs, financing programs, and direct equity stakes, the federal government is reshaping supply chains across pharmaceuticals, energy, critical minerals, and freight.

The initiative is intended to secure domestic production, reduce reliance on China, and ensure access to strategic inputs. For logistics leaders, the result will be increased reshoring activity, new demand for domestic infrastructure, and closer integration of supply chains with federal priorities.

At the same time, risks remain. The durability of these arrangements depends on political continuity, effective implementation, and the willingness of companies to partner with government under new terms.

In this evolving environment, logistics and supply chain professionals will need to monitor policy developments as closely as they do market trends. Supply chains are no longer shaped solely by efficiency and cost considerations. They are now integral to the nation’s industrial strategy.

The post Federal Industrial Partnerships and Supply Chain Realignment Under the Trump Administration: Pharmaceuticals, Semiconductors, Critical Minerals, and Energy appeared first on Logistics Viewpoints.

You may like

Non classé

Oil and Gas Digital Control Towers: Building the Data Infrastructure for Supply Chain Visibility

Published

37 minutes agoon

15 juillet 2026By

Oil and gas supply chains generate extraordinary volumes of data. Production assets, pipelines, refineries, terminals, vessels, railcars, trucks, maintenance systems, trading desks, finance platforms, and emissions reporting tools all produce information continuously. Yet in many organizations, that information remains locked inside functional systems built for specific departments and use cases.

Oil and Gas in the Supply Chain: A Strategic Framework for Building Resilient and Responsible Supply Chains.

This fragmentation is not simply an IT inconvenience. It is a business performance issue. Supply chain decisions in oil and gas rarely fit within one system boundary. A crude procurement decision may depend on refinery constraints, vessel availability, storage capacity, pipeline nominations, commercial exposure, and emissions considerations. A customer commitment may depend on terminal congestion, inventory quality, truck capacity, weather, and maintenance risk. When these domains are not connected, organizations make decisions with partial visibility.

Digital control towers are emerging as a practical response. Their purpose is not to add another dashboard to an already crowded technology landscape. The objective is to create a shared operating picture that brings together physical flows, asset status, constraints, inventories, risk, emissions, and commercial implications. In a business where volatility is persistent and capital intensity is high, better visibility must translate into better decisions.

From Fragmented Systems to Integrated Visibility

Oil and gas companies typically operate a large and diverse application environment. Production monitoring systems, SCADA, process historians, pipeline scheduling tools, refinery planning and scheduling systems, terminal management applications, marine scheduling platforms, rail logistics tools, truck dispatch systems, maintenance applications, procurement systems, inventory systems, commodity trading and risk management platforms, emissions reporting tools, and finance systems may all perform their core functions well.

The challenge is that no single one of these systems owns the end-to-end supply chain decision. A refinery scheduler may see unit constraints but not the full logistics cost of alternative crude movements. A trader may understand market exposure but not the near-term impact of terminal congestion. A maintenance team may understand asset risk but not the customer service or inventory implications of an outage. A logistics planner may see available capacity but not the financial value of reallocating that capacity across products, customers, or regions.

A digital control tower connects these domains into a more coherent view. The best control towers are not designed around the question, “What data can we display?” They are designed around the question, “What decisions must we improve?” That distinction matters. Oil and gas organizations already have more data than most teams can use. The value comes from organizing data around assets, products, customers, contracts, routes, cargoes, batches, units, and constraints.

The Oil and Gas Supply Chain Data Stack

A modern data stack for oil and gas supply chain operations can include operational technology, enterprise systems, and advanced analytics layers. Common components include:

SCADA and other operational technology systems for real-time asset and flow monitoring.

Process historians that capture high-frequency operational data from plants, pipelines, and refineries.

IoT sensors, edge devices, and condition monitoring systems across equipment and infrastructure.

ERP, enterprise asset management, transportation management, and procurement systems.

Terminal operating systems, laboratory information systems, and quality management platforms.

Commodity trading and risk management systems that track positions, contracts, pricing, and exposure.

Emissions monitoring and reporting systems that support regulatory and commercial requirements.

Data lakes, industrial data fabrics, AI engines, digital twins, and visualization tools.

This technology stack is only valuable when the data is contextualized. Raw sensor readings, inventory balances, maintenance work orders, shipment events, and commercial transactions do not automatically create insight. The system must understand what the data relates to: a specific pipeline segment, cargo, terminal, product grade, storage tank, refinery unit, customer order, supplier contract, or emissions source.

Without that context, companies may have data abundance but decision scarcity. With context, the same data can help leaders see cause and effect across the supply chain.

What a Digital Control Tower Should See

An effective oil and gas digital control tower should provide visibility across both the physical and commercial dimensions of the supply chain. At a minimum, this can include production volumes, pipeline flows, storage levels, LNG cargoes, refinery schedules, terminal capacity, vessel positions, rail and truck movements, product inventories by location, and maintenance risks.

It should also incorporate critical spare parts, customer commitments, emissions data, market exposure, weather events, and geopolitical disruptions where these factors can affect supply chain performance. The goal is not passive visibility. The goal is decision support. Leaders need to know what is moving, what is constrained, what is changing, what is at risk, and what action is required.

This is particularly important in oil and gas because physical flows and commercial exposure are deeply interdependent. A pipeline constraint can change the economics of a trade. A refinery unit issue can alter crude demand, product supply, and transportation plans. A vessel delay can affect storage availability, demurrage exposure, and customer delivery commitments. A methane anomaly or emissions compliance issue can affect market access, reporting obligations, and reputation.

Connecting Operational Truth to Commercial Decisions

The largest opportunity for digital control towers lies in connecting operational truth with commercial decision-making. Many companies still manage these domains through separate processes, handoffs, spreadsheets, and daily coordination calls. Those processes may work in stable conditions, but they are less effective when volatility increases or when multiple disruptions occur at once.

Production data should inform sales and transportation decisions. Pipeline constraints should inform trading and allocation choices. Refinery operations should inform crude procurement and product distribution. Terminal congestion should shape customer commitments and mode selection. Maintenance risk should influence inventory strategy and spare parts planning. Emissions data should be available to commercial teams when regulatory requirements or customer expectations affect market access.

When operational and commercial systems are disconnected, margin leaks through the gaps. The leakage may appear as demurrage, expediting, suboptimal crude slates, missed sales, excess inventory, underutilized capacity, avoidable emissions exposure, or poor customer service. A control tower cannot eliminate all of these issues, but it can help companies detect them earlier and evaluate response options more systematically.

AI, Predictive Intelligence, and Digital Twins

Artificial intelligence has a role to play, but it should be applied with discipline. The most valuable AI applications are tied to decisions with measurable financial, operational, safety, or compliance consequences. In oil and gas supply chains, these can include production forecasting, equipment failure prediction, pipeline constraint detection, crude slate optimization, refinery scheduling, marine estimated time of arrival prediction, demand forecasting, methane anomaly detection, spare parts planning, terminal congestion prediction, and weather impact modeling.

AI is most useful where speed, complexity, and uncertainty exceed what manual processes can manage effectively. It should not be deployed as a novelty layer on top of poor data. If the underlying data is inconsistent, poorly governed, or disconnected from business context, AI can accelerate confusion as easily as it can improve performance.

Digital twins extend the control tower concept by allowing companies to simulate alternatives before committing physical assets or capital. A digital twin can model pipelines, refineries, terminals, LNG cargoes, maintenance scenarios, energy systems, emissions profiles, weather disruptions, or supply-demand balances. Used well, these models help leaders test trade-offs: reroute a cargo, change a production plan, adjust inventory targets, defer maintenance, alter transportation modes, or evaluate emissions implications.

Cybersecurity and Data Integrity Are Foundational

As digital control towers become more central to supply chain operations, they also become part of the company’s critical infrastructure. This raises the stakes for cybersecurity, data governance, and operational resilience. A control tower that cannot be trusted will not be used in high-consequence decisions.

Core requirements include network segmentation, role-based access, multi-factor authentication, OT cybersecurity controls, continuous monitoring, data lineage, backup and recovery, incident response planning, and vendor access governance. These controls are not peripheral. They are part of the operating model for any control tower that connects operational technology, commercial systems, and enterprise data.

Data integrity is equally important. Leaders must understand the source of the data, how current it is, how it has been transformed, and whether it is fit for the decision at hand. High-quality supply chain data supports efficiency, resilience, regulatory reporting, emissions verification, customer transparency, capital access, commercial optimization, and supplier accountability.

Data Quality as a Strategic Differentiator

The next stage of oil and gas competition will not be determined only by who owns the best assets or who has the largest trading book. It will also be shaped by who can convert complex, cross-functional data into timely and trusted decisions.

Digital control towers are a key part of that shift. They can help companies move from fragmented systems and reactive coordination to integrated visibility and decision support. But the control tower is only as strong as the data infrastructure beneath it and the operating processes around it.

For supply chain, logistics, energy, manufacturing, operations, and technology leaders, the practical lesson is clear: start with the decisions that matter most, identify the data required to improve those decisions, build the contextual model, and govern the information as a strategic asset. In oil and gas, data quality is becoming more than an enabler. It is becoming a source of competitive advantage.

To explore the broader implications for oil and gas supply chain strategy, Download the full ARC Advisory Group white paper.

Download Oil and Gas in the Supply Chain.

The post Oil and Gas Digital Control Towers: Building the Data Infrastructure for Supply Chain Visibility appeared first on Logistics Viewpoints.

Non classé

IBM Shares Plunge as AI Infrastructure Spending Squeezes Enterprise Software Budgets

Published

13 heures agoon

14 juillet 2026By

IBM shares fell approximately 25 percent Tuesday after the company unexpectedly released preliminary second-quarter results that missed Wall Street expectations, raising concerns about how rapidly rising artificial intelligence infrastructure costs are reshaping enterprise technology budgets.

The decline erased nearly $68 billion from IBM’s market capitalization and represented the company’s largest one-day loss in market value. The stock was also headed for its steepest percentage decline since 1987.

IBM expects to report second-quarter revenue of $17.2 billion, an increase of 1 percent from the previous year, and adjusted earnings of $2.93 per share. Analysts had expected approximately $17.86 billion in revenue and earnings of $3.01 per share.

The company emphasized that these figures are preliminary and could change slightly when IBM reports its complete second-quarter results on July 22.

Customers Redirect Spending Toward Scarce Infrastructure

IBM CEO Arvind Krishna attributed much of the shortfall to an abrupt shift in customer capital spending during the final weeks of June.

Enterprise customers moved spending toward servers, storage and memory to secure supply-constrained infrastructure before anticipated price increases. That reprioritization reduced spending on IBM’s Z mainframes and the associated transaction-processing software.

“While we anticipated some supply chain related impact in our expectations, we did not anticipate the magnitude of the capex reprioritization,” Krishna wrote in a letter to investors.

IBM’s infrastructure revenue declined 7 percent, driven partly by weaker-than-expected performance in its Z mainframe business and the related software stack. Software revenue increased 5 percent, while consulting revenue was essentially unchanged.

The company also acknowledged internal execution problems. Several large transactions did not close during the quarter, and Krishna said IBM did not adapt quickly enough as customer priorities changed.

AI Spending Is Moving Between Technology Layers

The results do not necessarily indicate that companies are reducing their overall commitment to artificial intelligence. Instead, they show how spending is moving between different layers of the technology stack.

Companies facing shortages and rising prices for memory, servers and storage may accelerate infrastructure purchases while delaying software, consulting and modernization projects.

That shift has implications throughout the enterprise technology supply chain. Hardware manufacturers may experience accelerated demand, while software and services providers encounter delayed purchasing decisions even when customers continue pursuing AI programs.

IBM’s warning also pressured other technology stocks Tuesday, including ServiceNow, Salesforce, Microsoft and Oracle, as investors considered whether the spending shift extends beyond IBM.

IBM will provide its complete financial results and updated outlook on July 22

The post IBM Shares Plunge as AI Infrastructure Spending Squeezes Enterprise Software Budgets appeared first on Logistics Viewpoints.

Non classé

Container rates starting to spike on peak season rush – June 2, 2026 Update

Published

17 heures agoon

14 juillet 2026By

Weekly highlights

Ocean rates – Freightos Baltic Index

Asia-US West Coast prices (FBX01 Weekly) increased 1%.

Asia-US East Coast prices (FBX03 Weekly) increased 4%.

Asia-N. Europe prices (FBX11 Weekly) increased 3%.

Asia-Mediterranean prices(FBX13 Weekly) increased 1%.

Air rates – Freightos Air Index

China – N. America weekly prices increased 1%.

China – N. Europe weekly prices decreased 6%.

N. Europe – N. America weekly prices decreased 2%.

Analysis

Approaching 100 days since the start of the Iran war, despite periodic reports that an agreement that would open the Strait of Hormuz is near, the sides continue to exchange fire and sanctions, and the waterway remains closed.

For the container market, the closure has primarily meant upward pressure on freight rates via carriers passing on war-elevated fuel costs, which manifested in different ways on different lanes during the low demand months of March, April and most of May this year.

Join 70,000+ Supply Chain Experts Who Never Miss an Issue!

Start your week with the industry insights others miss.

« * » indicates required fields

Consent*

But peak season demand is kicking in early on east-west lanes, with reports of contracted shippers already seeing allocations reduced and premiums applied. So spot rates that climbed moderately – about 15% – across the ex-Asia lanes through mid-May GRIs to levels around 20% higher than a year ago, are starting to spike this week.

Weekly averages for last week were about level to close out the month, with transpacific rates at about $3,200/FEU to the West Coast and $5,000/FEU to the East Coast, and Asia – Europe prices at about $3,000/FEU to N. Europe and $4,400/FEU to the Mediterranean. But June 1st GRIs and PSS introductions have daily rates spiking from $1,000/FEU to $1,800/FEU so far this week on these trades, with additional significant increases announced for mid-month across these lanes as well.

Daily rates for Asia – Europe lanes have already surpassed peak season highs from last June/July, with transpacific still about $1,000/FEU short of last year’s brief, tariff frontloading-driven rate spike in July. Pre-existing war-related congestion in some tranship hubs, as well as rail congestion in Germany could also be a factor for rate pressure or delays for the relevant trades.

In trade war developments, IEEPA refunds – totalling about half of the total $166B paid – are on the way for importers whose customs entries had not already been liquidated, or finalized, by US Customs and Border Protection. But the Trump Administration indicated last week that it may challenge refunds for liquidated entries, arguing that the CBP is unauthorized to reliquidate and refund closed out entries without importer-specific court orders instructing it to do so.

Check out our full IEEPA tariff refund explainer and update page here.

This challenge, if successful, could mean that these importers would need to sue the government in trade court in order to get these duties refunded, and even if unsuccessful could mean a longer wait for impacted importers while the legal issues get sorted out. In the meantime, some trade law experts are advising importers with liquidated entries to file protests if the window hasn’t closed yet.

The trade war has resulted in lower or flat import volumes to the US alongside trade diversions driving volume increases between other countries as global players seek closer ties and trade growth beyond the US. Asia – Europe trade for example grew significantly last year and continues on pace so far in 2026. Even so, trade tensions between China and the EU may be increasing, as the EU considers legislation to curb subsidized imports.

Part of this issue relates to e-commerce imports to EU countries, which continue to grow significantly even as they flatten to the US and are reflected in diverging freighter capacity trends on these lanes. The EU will introduce a flat 3 EUR fee for low value imports starting in July, and a 2 EUR handling fee in November.

Though not as extensive as the US de minimis cancellation, these moves are likely to reduce EU e-commerce volumes arriving by air to some extent. Parcel carriers are warning that the system is still not ready for the new reporting requirements that will accompany the fee introductions, and warn of delays at European borders if these take effect in July.

Air cargo rates were about level on most major lanes this week, though the Freightos Air Index global benchmark – which is about even with April levels – remains more than 30% higher than before the start of the Iran war and year on year as capacity reductions and elevated jet fuel prices continue to impact price levels.

The post Container rates starting to spike on peak season rush – June 2, 2026 Update appeared first on Freightos.

Oil and Gas Digital Control Towers: Building the Data Infrastructure for Supply Chain Visibility

IBM Shares Plunge as AI Infrastructure Spending Squeezes Enterprise Software Budgets

Container rates starting to spike on peak season rush – June 2, 2026 Update

Walmart and the New Supply Chain Reality: AI, Automation, and Resilience

Why Sulfuric Acid Is Emerging as a Supply Chain Constraint in Copper

Container rates starting to spike on peak season rush – June 2, 2026 Update

Trending

-

Non classé1 an ago

Non classé1 an agoWalmart and the New Supply Chain Reality: AI, Automation, and Resilience

-

Non classé3 mois ago

Non classé3 mois agoWhy Sulfuric Acid Is Emerging as a Supply Chain Constraint in Copper

- Non classé1 mois ago

Container rates starting to spike on peak season rush – June 2, 2026 Update

- Non classé11 mois ago

13 Books Logistics And Supply Chain Experts Need To Read

- Non classé9 mois ago

Ex-Asia ocean rates climb on GRIs, despite slowing demand – October 22, 2025 Update

- Non classé6 mois ago

Container Shipping Overcapacity & Rate Outlook 2026

- Non classé5 mois ago

Ocean rates ease as LNY begins; US port call fees again? – February 17, 2026 Update

-

Non classé1 an ago

Non classé1 an agoAmazon and the Shift to AI-Driven Supply Chain Planning